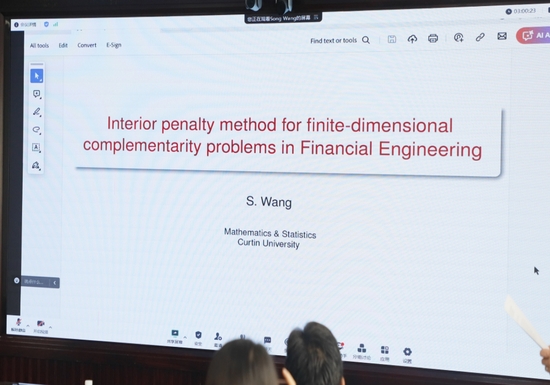

講座題目 | An interior penalty method for finite-dimensional complementarity problems in Financial Engineering | ||

主辦單位 | EON体育4开户 | 協辦單位 | 應用統計系 |

講座時間 | 6月22日09:00-10:00 | 主講人 | Song Wang (汪崧) |

講座地點 | 行政樓1308室 | ||

主講人簡介 | Song Wang(汪崧)教授,澳大利亞科廷大學(Curtin University)數學與統計系教授。1982年在武漢大學獲得學士學位,1989年在愛爾蘭都柏林聖三一EON4(Trinity College Dublin)獲得博士學位,曾在愛爾蘭都柏林的高科技公司--Tritech有限公司工作💆🏿♂️,先後任澳大利亞新南威爾士大學,科廷科技大學和西澳大利亞大學教授🧑🏿🏭。主要從事偏微分方程的數值解🐭,數值優化和最優控製,金融衍生品定價模型的理論和數值算法等研究🌠。在SIAM Journal of Optimization, SIAM Journal of Numerical Analysis, Numerische Mathmatik, Automatica, IEEE Transactions on Neural Networks, IMA Journal of Numerical Analysis, Reports on Progress in Physics, Journal of Computational Physics, Biomaterial, Journal of Optimization Theory and Applications, Journal of Global Optimization等國際SCI知名雜誌上發表學術論文150余篇🎍。同時,汪教授還擔任多個國際知名SCI雜誌的主編,副主編以及編委。 | ||

講座內容簡介 | In this work we propose and analyse an interior-point based penalty method for a finite-dimensional large-scale linear and nonlinear complementarity problem (CP) arising from the discretization of an infinite-dimensional obstacle problem in classic and financial engineering. In this approach, we approximate the CP by a nonlinear algebraic equation containing a penalty/barrier term with a penalty parameter mu. The penalty equation is shown to be uniquely solvable. We also prove that the approximate solutions converge to the exact one. A smooth Newton method is proposed for solving the penalty equation and it is shown that the linearized system is reducible to two decoupled subsystems. Extensions of this method to other types of CPs are will also be presented. Numerical experimental results using some non-trivial test problems will be presented to demonstrate the rates of convergence and accuracy of our methods. | ||

澳大利亞科廷大學汪崧教授為我校師生作學術報告

推進EON4科研國際交流與合作,6月22日數理與統計邀請澳大利亞科廷大學汪崧教授為廣大師生作了題為“Interior penalty method for finite-dimens-ional complementarity problems in Financial Engineering”的學術報告。

汪崧教授從有限維互補問題出發🍖,深入探討了利用內罰函數法解決由經典與金融工程中無限維障礙問題離散化產生的大規模線性與非線性互補問題。詳述了通過包含懲罰/障礙項的非線性代數方程近似互補問題的方法。為解決懲罰方程🌃,汪崧教授重點介紹了課題組提出的一種新的光滑牛頓法,並指出線性化系統可簡化為兩個獨立子系統。此外,他還討論了該方法在其他類型互補問題中的擴展應用。報告通過展示多個非平凡測試問題的數值實驗結果,驗證了所提方法的收斂速度與準確性🧑🏽🦱,同時分享了該方法在金融工程領域中的實際應用案例🎮。此次講座不僅加深了師生們對內罰函數法在解決有限維互補問題上的理解🙏🏼,更為相關領域的研究與應用提供了寶貴見解。